Did we miss something?

... about investment, data centers, and AI

The most staggering figures are being announced, with talk of hundreds of billions, a world populated by robots, a super artificial intelligence capable of generating its own knowledge that would be within our reach, ChatGPT valued at $500bns etc… Let's review some data and make some remarks..

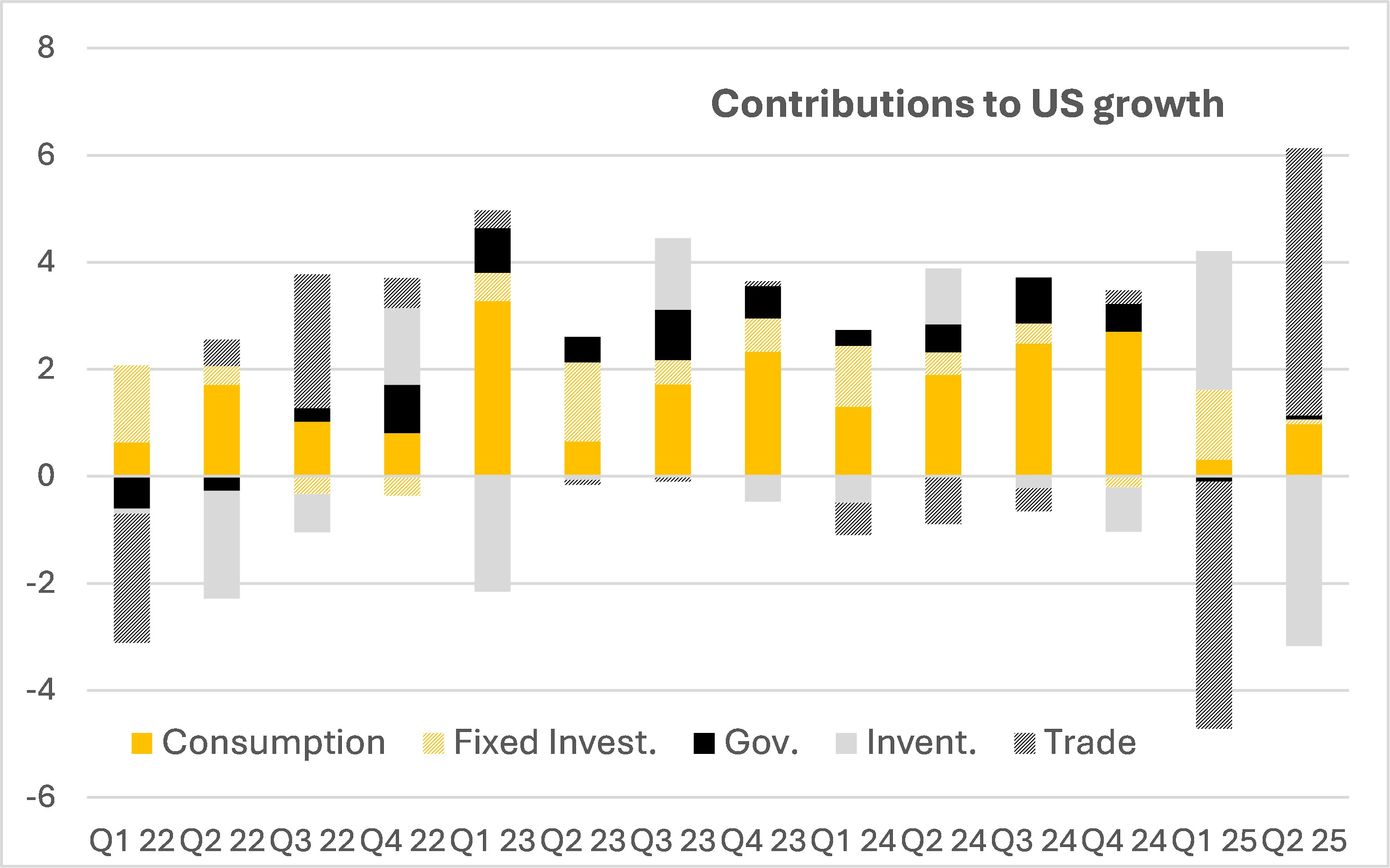

The latest investment figures in the United States have been rather disappointing, with an average contribution to growth of 0.4 percentage points over the past four quarters, compared to an average of 65 basis points since 1950 and even 75 basis points since 2010. So what investment boom? We need to delve into the details. But the first observation is this: so far, the boom in AI and data centers has had no visible impact on total investment, which itself represents only 18% of GDP, including the energy and mining sectors.

Sources: BEA, SARIM

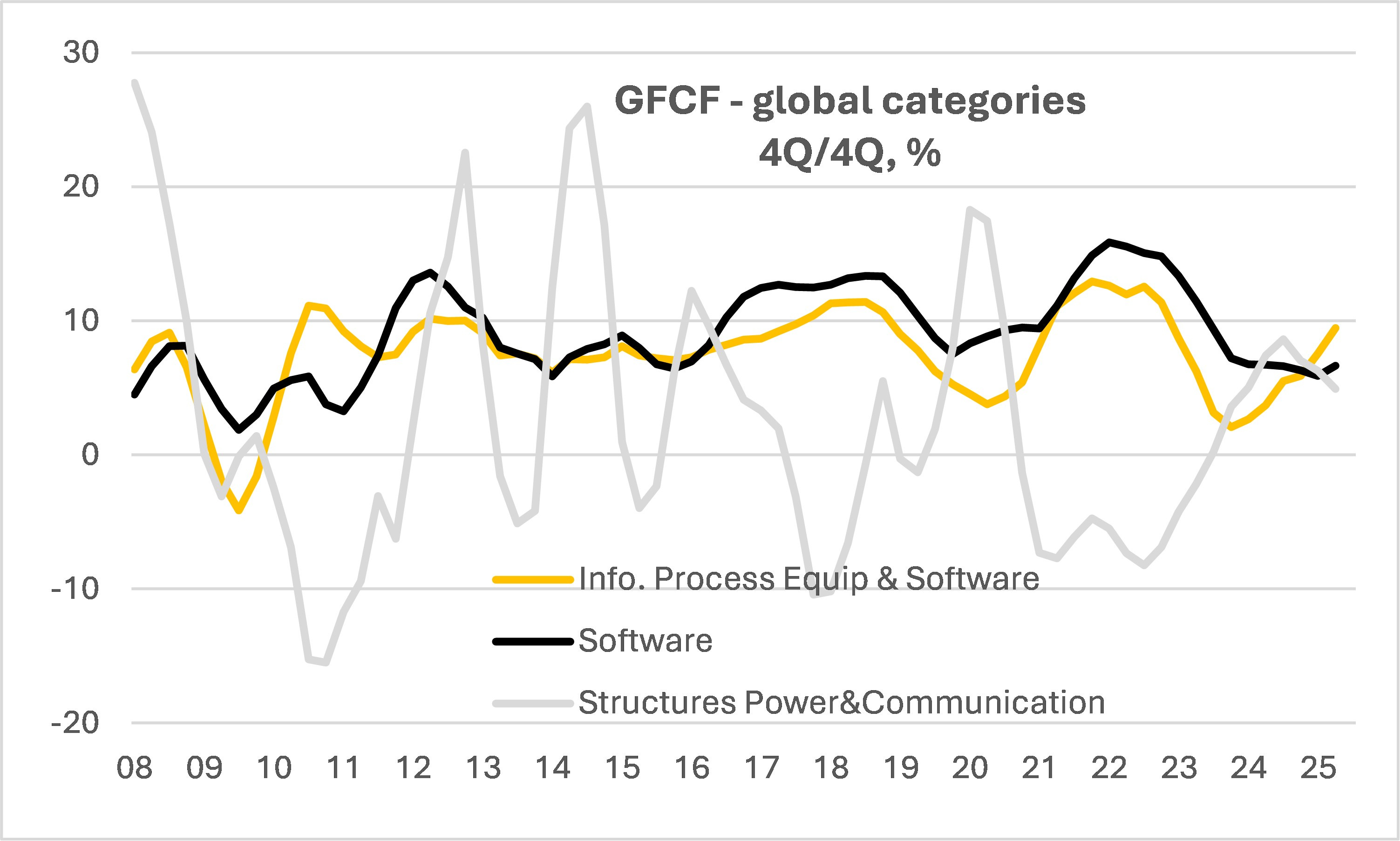

The first step is to disregard residential investment, which is indeed in a slump and still below its 2007 levels in real terms, barely above 2019 levels. Commercial real estate is also still depressed and contracting... Ultimately, three categories interest us: buildings (structures) in the Energy and Communication category, the Software category, and the Information Process, Equipment & Software one. The Bureau of Economic Analysis does not publish figures dedicated to data centers and AI, but we can assume that related expenditures end up in one of these categories.

Sources: BEA, SARIM

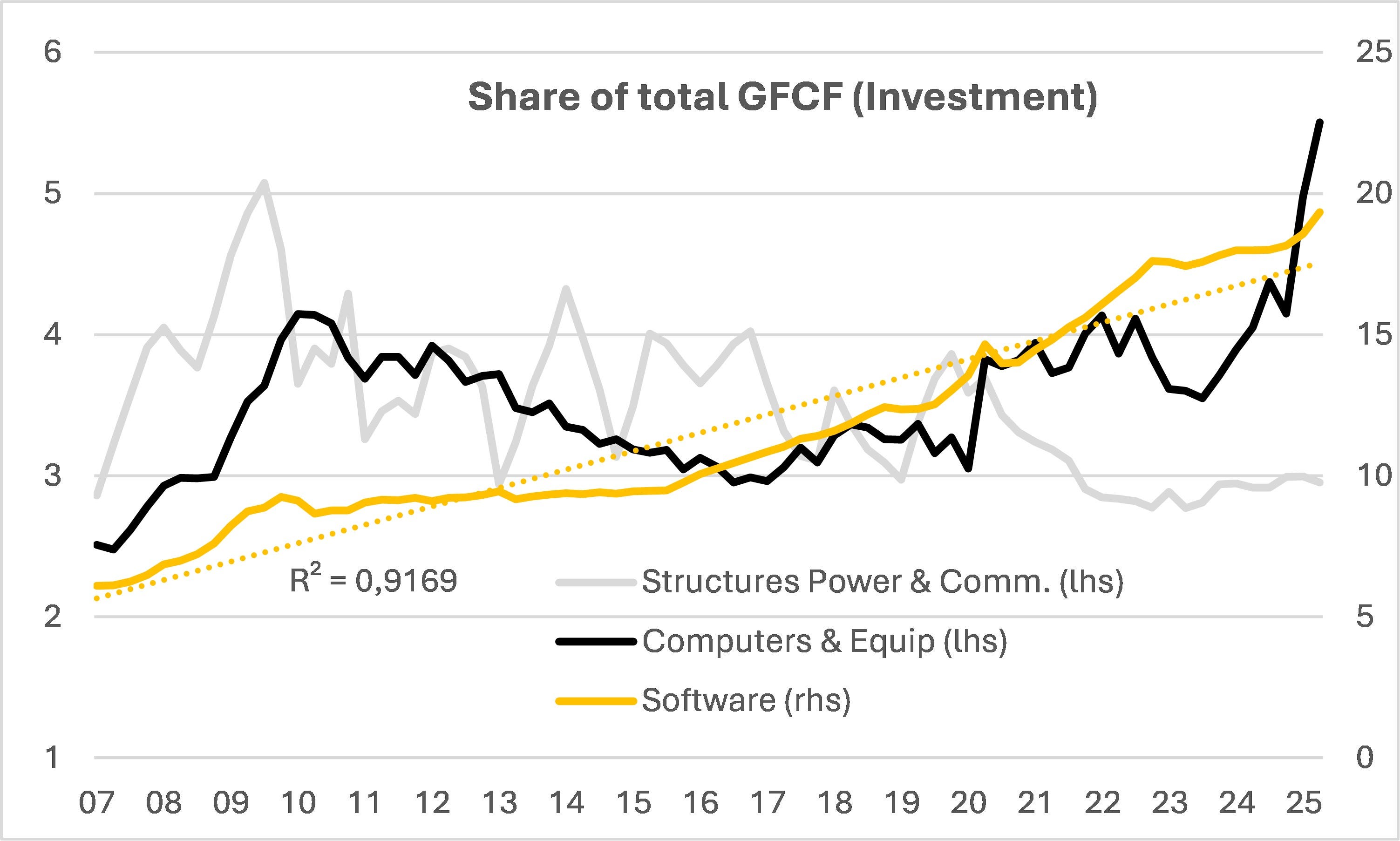

All these sub-categories of investment are experiencing strong growth, but how much do these sectors ultimately weigh in total investment? A little over $1.2 trillion (in real terms), or 30% of total non-residential investment—and thus 6% of GDP. Not all these sums are linked to data centers and AI; for decades, investment in software and computer and telecommunications equipment has been taking market share from manufacturing, agricultural, mining and other investments in the total. The graph below shows us the linearity... However, and this is our second point, we are indeed seeing a recent acceleration: software is deviating from linearity, and equipment is breaking its high point...

So, to answer our initial question, for now, at an aggregated level, we haven't missed anything yet, but the phenomenon needs to be closely monitored.

Will this dynamic continue as it begins to show in investment figures? For the coming months, certainly... Nevertheless, the question of the profitability of these investments, currently funded at a loss by tech giants and various sovereign funds, is now openly raised...

Companies and individuals will pay if the tools and processes offered allow them to either reduce their costs, create new products, or improve the quality of existing products and pass the cost on to consumers. Some say that using AI is no longer an alternative to surviving and maintaining market share, labor value, etc.... May be. Internal sources at ChatGPT—we quote Reuters here—indicate that currently, less than 10% of users pay a monthly subscription ranging from $20 to $200. OpenAI is valued at $500 billion. Calculations show that to justify this amount, based on fundamentals comparable to other tech giants, revenue must reach $225 billion by 2030, compared to $20 currently. Nividia is expected to reach “only” $350 billion at that time. This kind of calculation is also true for the other Hyperscalers. Add the "threats" of open source on the one hand—and many coding professionals work in open source—but also the complexity of implementing projects at the corporate level. And today, early struggles and glitches mean 42% of companies have scrapped AI deployments this year, up from 17% in 2024, according to S&P Global. In addition to the complexity of implementing enterprise-scale projects, there are questions about the energy required for the advent of these visions and their financing, as the pockets of current funders are not infinite either. We are talking about a supposed total need of $3 trillion according to (bullish) investment banks studies.

In other words, it is a gigantic bet based on beliefs in technological progress—the advent of a "super intelligence"—and the widespread paid use of AI by the public and businesses. It is quite normal for those who would benefit from it to present it as a certainty. The long-term interest of generative AI is not in question, of course; we used AI already 30 years ago in our PhD—in economics, on Forex, to model crowd behavior through agents, and we continue in this direction—but rather that of the rhythm of the adoption cycles, the past and future winters of these AI-related technologies – we lived through one between the end of the 90’s and beginnings of the 2010’s- and investment monetization.

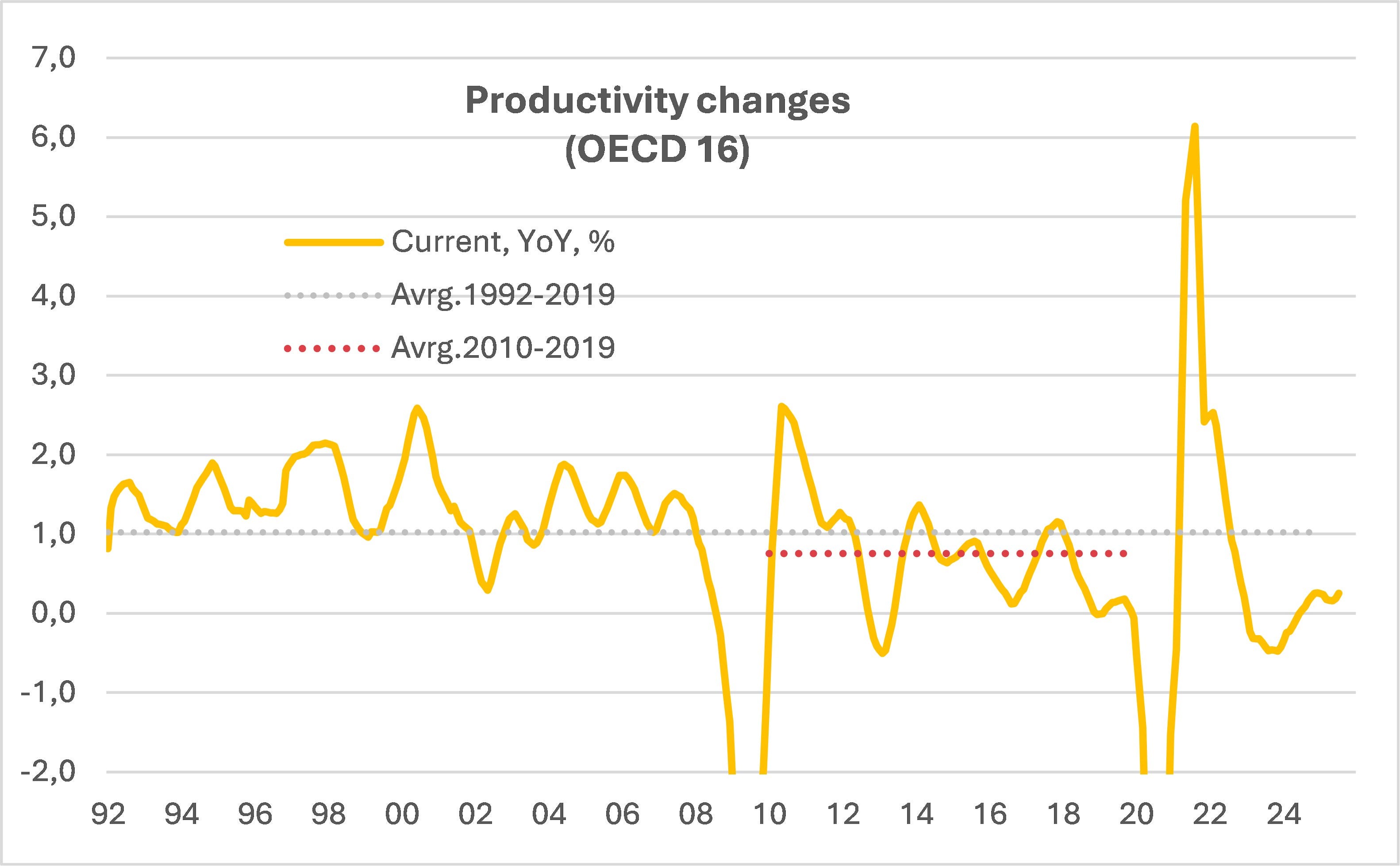

And to return to macroeconomics, these investments and developments that happen at a micro level, must have an impact on productivity at some point... productivity that needs to be observed for the entire economy, as the most significant impact is expected in services. For now, as shown in the graph below, and quite unsurprisingly, the productivity revolution is still to come, if it comes at an aggregated level, according to OECD data... If those gains do not accelerate, the technology will only impact the distribution in wealth rather than augmenting the size of the cake, the total wealth.

Sources: OECD, SARIIM